Trends in qualified retirement plans: Should I have a 401(k) or SIMPLE IRA?

Saving for retirement is imperative. One of the best ways to begin is implementing a tax-favored 401(k) plan or SIMPLE IRA plan. Picking the right plan at the right stage of your dental career, however, will go a long way towards creating a balance sheet that is well-rounded, protected, and balanced.

It’s a frequent conversation with clients and prospective clients alike. “What kind of retirement plan should I have for my office? My CPA says I should implement a 401(k).”

I wish the answer was as straightforward as this, but it really depends on several factors.

While the 401(k) plan has been around since 1974, the SIMPLE IRA plan (Savings Incentive Match Plan for Employees) was just introduced in 1996 as part of the Small Business Job Protection Act. The intent of this plan was to provide small employers (100 employees or fewer) a simplified platform to offer retirement savings opportunities to employees. Removing some of the administrative costs and record keeping burdens that are inherent in other qualified retirement plans, SIMPLE IRA plans have become quite popular in dental offices across the country. There are several other types of plans, but my experience has been that most offices have chosen to implement either a 401(k) or a SIMPLE IRA.

Choosing between a 401(k) plan and a SIMPLE IRA plan hinges on four factors:

- Maximum current-year contribution / tax deduction

- Cost of operating

- Liquidity

- Future tax liability

Let's take a look at each of these factors individually, along with how they relate to my financial planning philosophy of "optimal balance." After further review, you might find the answer varies depending on the stage of your practice as well as your long-term goals.

Maximum current-year contribution / tax deduction

The 401(k) plan is the clear winner in this category. It allows annual employee deferrals (tax-deferred contributions) of up to $18,000. In contrast, $12,500 is the maximum deferral for a SIMPLE IRA plan. What's more, dentists can add a profit-sharing component to their 401(k) plans, thereby increasing the maximum allowable contribution to $54,000.

The bottom line: With its higher contribution limit, a 401(k) plan affords a practicing dentist a significantly higher current-year tax deduction.

Cost of operating

When we consider the operating costs for each plan alone, SIMPLE IRA plans are more attractive because they carry lower administrative costs. Much of the higher costs of 401(k) plans come from third-party administrator fees for services, which include but are not limited to the annual filings of the annual reports to the IRS and Department of Labor (DOL).

Conversely, a SIMPLE IRA plan generally does not require a third-party administrator because each plan participant’s account is automatically invested in each participant-owned (SIMPLE) IRA annuity contract or custodial account. A model plan document is also available from the IRS and may be used instead of a “formal,” custom-designed or prototype-plan document. Also, there are generally no annual filings with the IRS or DOL, and nondiscrimination requirements are generally not an issue.

Liquidity

Liquidity is one of the single most important financial virtues to grasp and embrace. For this reason, I will spend more time on this topic than any other in this article.

Over the past 25 years, I have had the privilege of reviewing the balance sheets of practicing dentists from coast to coast. If I had to pick one planning challenge that I see most often, it’s the problem of what I call being “retirement plan poor.” This is not to say that retirement plans are bad—not even close. My point is that I have seen many balance sheets of dentists that are so heavily weighted towards their office-qualified retirement plans that they have little to no personal liquid assets available. Because early distributions from both 401(k) and SIMPLE IRA plans (before age 59½) are both fully taxable and can result in penalties, this has put many dentists in a liquidity crunch at times where cash might be needed for an emergency, a business opportunity, or a large purchase.

Let's look at an example to clarify this concept.

Example: "Retirement plan poor and resulting liquidity deficiency"

What if you are presented with an investment or business opportunity that you feel is a must? What about a large purchase you would like to make? Worse yet, what if you have an emergency need for funds? And what if although you have a positive net worth, it's mostly tied up in you retirement plan and real estate (illiquid)? To acquire every $100,000 you need, here is what it would cost you.

Withdrawal from retirement plan

$166,667 withdrawal

($50,000) taxes at 30% (estimated)

($16,667) penalty at 10% (may apply)

______________________________

$100,000 gained

So, for every $100,000 needed, $66,667 could be lost to taxes and penalties if withdrawn from a qualified retirement plan, such as a 401(k), SIMPLE IRA, etc.

The lesson: Make sure there is "balance" in you balance sheet. After tax, nonqualified liquidity could be very important!

Some may argue that there are other avenues to take besides a pure withdrawal from your retirement plan, e.g., loans, hardship withdrawals, etc. Some plans don’t offer these provisions at all, and plans that do have strict IRS guidelines to follow. It’s also important to note that there are anti-alienation rules in place that prevent using qualified retirement accounts as collateral, whereas other nonqualified accounts can be pledged or even borrowed against at some investment firms.

I also see many dentists whose protection portfolios are underfunded, all while they are making maximum contributions to their retirement plan. Your protection portfolio is made up of products like life, disability, malpractice and personal liability insurance. These products are designed to protect your balance sheet against unpredictable perils that can derail even the best-laid financial plans. Given the unpredictable nature of these risks, as well as the reasonable predictability of your retirement age range, your protection portfolio is the foundation of your balance sheet.

A word on "optimal balance"

One of the hallmarks of my financial planning philosophy is what I call "optimal balance." Optimal balance is the concept of constructing your entire financial portfolio with diversity as a building block. Achieving this optimal balance puts you in the best position to maximize your portfolio’s potential, regardless of ever-changing personal and economic events. This holds true when it comes to choosing and funding a retirement plan, too, and the maximum funding of your 401(k) plan (or even SIMPLE IRA plan) without having proper nonqualified (after-tax) investments is a recipe for becoming unbalanced and possibly “retirement plan poor.” Given the importance of liquidity and balance, I often recommend SIMPLE IRA plans to start, then moving to 401(k)/profit-sharing plans as excess cash flow develops. (A SIMPLE IRA plan generally is easier to terminate than a 401(k)/profit-sharing plan.)

Future tax liability

Tax-deferred earnings are one of the key benefits of qualified retirement plans. Tax deferral is an incredible building block for compounding returns, but it’s also important to note the word "deferral." There will come a day when the tax bill will be due on these funds.

I often ask my clients, “Do you think taxes are going up or down in the future?” The overwhelming majority of clients say they believe taxes will go up. The correct answer is that we don’t really know what will happen. We do, however, have the advantage of historical data.

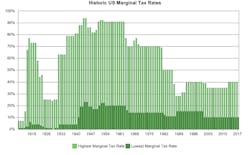

The chart below illustrates both the highest and the lowest marginal tax rates from 1913 to 2017.

Figure 1: Historic marginal US tax rates

Source: US Treasury Department—Internal Revenue Service 2017. Values shown are not guaranteed to reflect values as of the date shown. Please carefully review the Disclosure page (below) for important information concerning valuation and other matters. The Guardian Life Insurance Company of America (Guardian), New York, NY. Reprinted with permission.

Historically, the tax climate has been cyclical at best…and politically motivated at worst. Given this uncertainty, the principle of optimal balance is important here. Having both qualified (taxable) assets as well as nonqualified (nontaxable) assets puts you in position to access funds from whichever account is more financially advantageous at the time of withdrawal. If taxes are historically high, withdraw funds from your nonqualified accounts. If you are in a period of low taxation, withdraw funds from your qualified accounts, which includes 401(k) plans and SIMPLE IRA plans. The key here is the power of choice.

As with many financial decisions, the situation isn’t black and white. A practice owner’s specific financial circumstances must be weighed carefully in order to choose the right path. Unfortunately, current-year tax benefits are oftentimes the singular data point used in making this decision, and that can have negative financial implications in the future. It’s also important to note that there are other types of plans that may be appropriate for your situation, such as ROTH IRAs, SEP plans, or defined-benefit plans.

The takeaway

Saving for retirement is imperative. One of the best ways to begin is implementing a tax-favored 401(k) plan or SIMPLE IRA plan. Starting your retirement savings as early as possible can also make reaching your long-term financial goals a more feasible proposition. Picking the right plan at the right stage of your practice, however, will go a long way towards creating a balance sheet that is well-rounded, protected, and balanced.

Andy Upchurch, RHU, REBC, is the president of Continuum Financial Solutions. Based in Charlotte, North Carolina, Andy travels throughout the United States as a dental- and medical-specific financial advisor. Andy can be reached at (317) 701-2226 or [email protected]. Read more about Andy and the type of work he provides for his clients at continuumfinancialsolutions.com.

Additional articles

Not your father's disability insurance

"What's going on with the market?!" Advice for dentists in a volatile financial climate

5 ways dentists can manage personal wealth during the Trump presidency

Andy Upchurch is a monthly columnist in the Apex360 e-newsletter.

Author disclosures:

Registered Representative and Financial Advisor of Park Avenue Securities, LLC (PAS), 4201 Congress Street, Suite 295, Charlotte, NC 28209. Securities products/services and financial advisory services offered through PAS, a registered broker-dealer and investment advisor, (704) 552-8507. Financial Representative, The Guardian Life Insurance Company of America, New York, NY. PAS is an indirect, wholly owned subsidiary of Guardian. Continuum Financial Solutions is not an affiliate or subsidiary of PAS or Guardian. PAS is a member of FINRA, SIPC.

Material discussed is meant for general informational purposes only and is not to be construed as tax, legal, or investment advice. Although the information has been gathered from sources believed to be reliable, please note that individual situations can vary. Therefore, the information should be relied upon only when coordinated with individual professional advice. This material contains the current opinions of the author but not necessarily those of Guardian or its subsidiaries and such opinions are subject to change without notice. 2017-38779 Exp 04/19.

Editor's note: This article first appeared in the Apex360 e-newsletter. Apex360 is a DentistryIQ partner publication for dental practitioners and members of the dental industry. Its goal is to provide timely dental information and present it in meaningful context, empowering those in the dental space to make better business decisions. Subscribe to the Apex360 e-newsletter here.

For the most current dental headlines, click here.

About the Author

Andy Upchurch, RHU, REBC

President, Continuum Financial Solutions

Andy Upchurch, RHU, REBC, is the president of Continuum Financial Solutions. Based in Charlotte, North Carolina, Andy travels throughout the United States as a dental- and medical-specific financial advisor. Andy can be reached at (317) 701-2226 [email protected]. Read more about Andy and the type of work he provides for his clients at continuumfinancialsolutions.com.

Updated January 30, 2016